If you’ve ever searched for a credit card $200 bonus easy approval, you’re not alone. I remember feeling both excited and skeptical the first time I saw these offers. “Is this really legit?” That question stuck with me — and if you’re here, it’s probably on your mind too.

The good news? These offers are real — and when used correctly, they can be one of the easiest ways to earn extra cash back from everyday spending.

Let me walk you through everything in a clear, honest, and practical way.

What Does “Credit Card $200 Bonus Easy Approval” Really Mean?

When I first explored these offers, I realized that most $200 bonus credit cards follow a simple structure:

- You apply and get approved

- You spend a certain amount (usually $500–$1,000) within 3 months

- You receive a $200 bonus

This is called a welcome bonus or sign-up bonus.

Many banks design these offers to be achievable. In fact, some of the easiest bonuses require only $500 in spending, which makes the “easy approval” aspect feel more realistic — especially for people with fair to good credit.

Why These Bonuses Are Popular Right Now

From my experience, these offers have become more competitive in recent years. Banks are trying to attract new customers, so they provide:

- Lower spending requirements

- No annual fee options

- Straightforward cash back rewards

This is why you’ll often see variations like:

- $300 credit card bonus no annual fee

- $500 credit card bonus no annual fee

- Even premium offers like $1,000 credit card bonus

But here’s the important part: higher bonuses usually come with higher spending requirements or stricter approval criteria.

Understanding Different Bonus Tiers

Entry-Level Bonuses ($200 – $300)

These are the most beginner-friendly.

- credit card $200 bonus easy approval

- $300 credit card bonus no annual fee

Best for:

- First-time applicants

- People with average credit scores

- Low monthly spending

Most of these require $500–$1,000 spend in 3 months, which is manageable for everyday expenses.

Mid-Tier Bonuses ($500 Range)

You might come across:

- $500 credit card bonus no annual fee

- u.s. bank credit card $500 bonus

These are slightly harder to earn but still accessible.

What I’ve noticed:

- Spending requirement increases ($2,000–$4,000 typical)

- Approval may require stronger credit

Some banks like U.S. Bank also offer u.s. bank credit card pre approval tools, which help you check eligibility without impacting your credit score.

Premium Bonuses ($1,000 and Above)

These include:

- $1,000 credit card bonus

- $1,000 credit card bonus no annual fee (rare but occasionally available)

Important reality:

These are not “easy approval” offers.

They often require:

- Excellent credit

- High spending thresholds

- Sometimes annual fees

I always recommend beginners start with $200–$300 bonuses before chasing these.

Real Examples of $200 Bonus Offers (Simplified)

From reviewing multiple offers, here’s what I consistently see:

- Spend $500 in 3 months → Earn $200 cash back

- No annual fee

- Flat-rate rewards (like 1.5%–2% cash back)

Some cards even offer:

- Intro APR periods

- Extra category bonuses (groceries, travel, etc.)

This structure makes them one of the most practical financial tools when used responsibly.

Step-by-Step: How I Approach These Offers

Step 1: Check Your Credit Score

Before applying, I always check where I stand. “Easy approval” still usually means:

- Fair to good credit (650+ recommended)

Step 2: Use Pre-Approval Tools

Banks like U.S. Bank offer:

- u.s. bank credit card pre approval

This helps avoid unnecessary hard inquiries.

Step 3: Choose the Right Card

I focus on:

- No annual fee

- Low spending requirement

- Useful rewards

Step 4: Plan Your Spending

This is crucial.

I don’t spend extra — I simply:

- Use the card for groceries

- Pay bills

- Cover routine expenses

Step 5: Pay Balance in Full

This is non-negotiable.

Interest charges can cancel out your bonus completely.

What NOT to Do (Very Important)

I’ve seen people make these mistakes — and they can cost you money:

Don’t overspend just to earn the bonus

Don’t miss the 3-month deadline

Don’t carry a balance with high interest

Don’t apply for multiple cards at once

Even with credit card $200 bonus easy approval, responsible usage matters more than the bonus itself.

Understanding Credit Limits (Example: U.S. Bank Cash+)

A common question I get is about limits, especially:

- u.s. bank cash+ visa signature card credit limit

From what I’ve observed:

- Visa Signature cards typically start around $5,000+ limits

- Actual limits depend on your:

- Income

- Credit score

- Debt level

Higher limits can improve credit utilization — but only if managed wisely.

Common Misconceptions (Let’s Clear These Up)

“Easy approval means guaranteed approval”

Not true. Approval still depends on your credit profile.

“Bonuses are free money”

Technically yes — but only if you avoid interest.

“Higher bonus is always better”

Not always. A $200 bonus you can easily earn is better than a $1,000 bonus you can’t.

When NOT to Apply (Important Warning)

There are times when you should pause and not chase these offers:

If your credit score is very low

If you already have high credit card debt

If you struggle to manage monthly payments

If you’re applying for a loan soon

In these cases, improving your financial health should come first.

Emotional Side: You’re Not Alone

I understand how confusing this space can feel.

There are so many offers:

- $500 credit card bonus no annual fee

- $1,000 credit card bonus

- credit card $200 bonus easy approval

It’s easy to feel overwhelmed.

But here’s the truth:

You don’t need the “best” card — you need the right card for your situation.

Start small. Stay consistent. Build confidence.

What to Expect After You Earn the Bonus

Once you complete the spending requirement:

- Bonus usually posts within 1–2 billing cycles

- You can redeem it as:

- Statement credit

- Bank deposit

- Rewards points

Long-Term Impact on Your Credit

Used correctly, these cards can actually help:

Build credit history

Improve utilization ratio

Increase total available credit

But misuse can hurt — so discipline matters.

Trusted Resources

Consumer Financial Protection Bureau (CFPB) – Credit card basics and consumer rights

Federal Reserve – Credit usage and financial behavior insights

Chase Official Website – Credit card terms and welcome bonus details

Capital One Official Website – Credit card offers and rewards details

Wells Fargo Official Website – Credit card features and bonus offers

U.S. Bank Official Website – Pre-approval tools and credit card offers

Submit Your Story

Have you tried earning a credit card $200 bonus easy approval?

I’d genuinely love to hear your experience:

- Which card worked for you?

- Was the bonus easy to earn?

- Any mistakes you learned from?

Sharing real experiences helps others make smarter decisions.

FAQ

What is the $200 cash bonus credit card?

A $200 cash bonus credit card is a card that offers a $200 welcome bonus after you meet a simple spending requirement—usually $500 to $1,000 within the first 3 months. Many popular cards from banks like Chase, Capital One, and Wells Fargo offer this type of bonus with no annual fee, making them one of the easiest and most accessible rewards.

What is the easiest credit card to get instant approval?

The easiest credit cards to get instant approval are typically designed for people with fair to good credit. These include entry-level cash back cards and some secured credit cards. Many issuers like Capital One, Discover, and U.S. Bank also offer pre-approval tools, which let you check your chances without affecting your credit score.

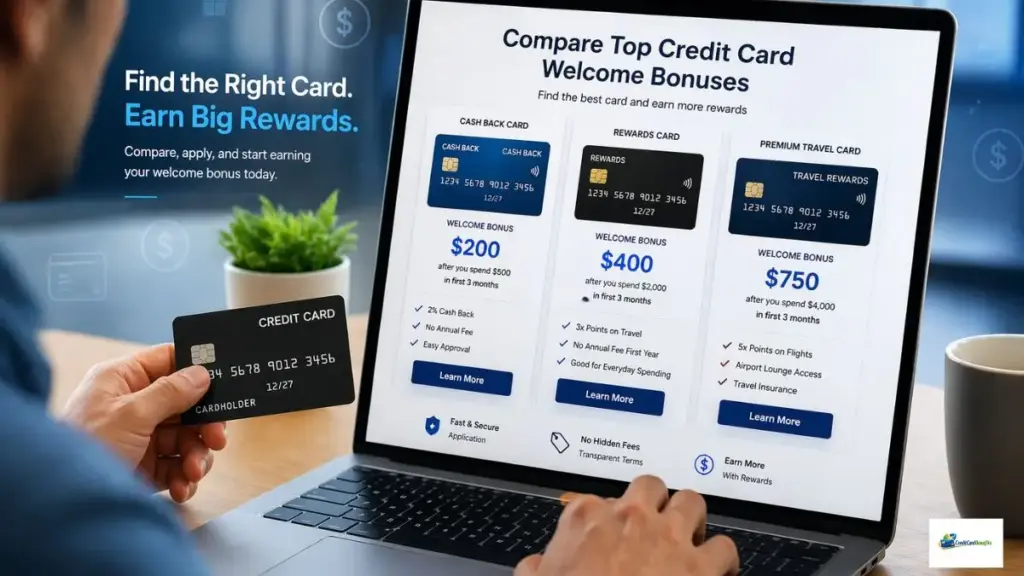

What is the $400 bonus credit card?

A $400 bonus credit card usually requires a higher spending threshold, often around $2,000 to $3,000 within the first few months. These offers are common with mid-tier rewards cards from issuers like Chase and American Express. Approval typically requires a good to excellent credit score.

What is the $750 welcome bonus credit card?

A $750 welcome bonus credit card is a high-value offer typically found on premium travel or rewards cards. These bonuses often require significant spending, such as $4,000 or more in the first 3 months. They are usually offered by issuers like Chase (Ultimate Rewards) or American Express and are best suited for users with strong credit and higher monthly spending.

What credit card has the best welcome bonus right now?

The best welcome bonus depends on your spending habits and credit profile. Currently, premium travel cards often offer the highest bonuses (sometimes worth $750 or more), while $200–$300 bonus cards remain the best option for easy approval and low spending requirements. It’s important to choose a card that matches your financial situation rather than just chasing the highest bonus.

Final Thoughts: Is It Worth It?

From my personal experience, yes — absolutely.

If you:

- Choose the right card

- Spend responsibly

- Pay on time

credit card $200 bonus easy approval

Then these bonuses can be one of the simplest ways to earn extra money from expenses you already have.